Tuesday, May 16, 2000

Massachusetts Software and Internet Council Spring Membership meeting

Yesterday I attended the Massachusetts Software and Internet Council's Spring Membership meeting at the Newton Marriott. We had two very interesting speakers, Thomas Willmott, president and CEO of the Aberdeen Group, and Alan Webber, co-founder of Fast Company. I have separate items on each of their speeches, below.

These speech writeups are long, but I thought both speakers said things of value to you, my readers, so I included most of my notes. (If you don't have time to read them all, read a little each time you come back and find out I haven't added more to this site yet... I seem to vary from daily to weekly additions depending upon the week.)

In addition, on display were the entries in the annual Visual Communications Contest. Each year, starting 4 years ago, the Council partners with Boston University to provide graphic design students with real-world experience and participating companies with exposure to up-and-coming design talent. This year, 30 senior and graduate-level students showed their projects, usually a corporate identity implemented both on letterhead and on web sites.

Some of the contest entries, print and web

Thomas Willmott of Aberdeen Group speaks about incubators

Tom is president and CEO of Aberdeen Group, a provider of consulting and market strategy advice to IT suppliers and investors. His speech was entitled: "Incubators: The Internet Economy Meets Venture Investing".

Thomas Willmott

Here are some of his points:

"Getting money today is like shooting fish in a barrel." "Getting money today is like shooting fish in a barrel." The move to establish market share and dominance quickly, enhanced by IPO money, is a tremendous change from the old days.

Because of this need for IPO money, capital markets have tremendous impact. Since being dominant is the key factor to valuation, the ability to move quickly and get funds is important.

The notion of an incubator is to surround a company with the stuff to transition from seed funded to mature company faster, to get market dominance sooner.

In the technology trends, more and more bandwidth is important. New England companies played a pivotal role here.

3Com's acquisition of General Robotics for 56Kb modem technology (over the old 33Kb) was "almost a round-off error" in speed increase by today's standards.

In funding, bandwidth is also king, but here it is bandwidth in how many deals the investors can look at and evaluate in the time they have. Venture capital management capacity is the limiting factor.

"Equity, equity, equity." Everything is equity these days. On the West Coast, "if you go to the dentist's office they want equity -- cash is no longer king."

Old investors were angels, VC's, and Friends & Family. Now, you have to add Institutions, Corporate Investors, and Venture Accelerators.

Incubators (an accelerator?) had exponential growth in the second half of 1999.

There is a lack of differentiation among incubators, and the rush and high valuations have left many with questionable portfolio components.

Three primary incubator business models: Long Term Ownership, Short Term Investment, Hybrid.

Long Term model assumes the original investors will be the primary financier long term. $500K-$1M seed financing with a 30-70% equity position, and a goal of IPO or merger/acquisition.

Short Term assumes just seed funding, then grooming for outside financing and a financial return to the incubator at a liquidity event. $250K-$500K seed, 10%-30% equity, goal of Series A or B financing. On the West Coast there are many high volume, high churn incubators to see as many deals a possible and find those that might make it. Those that don't look good enough after 6 months are let go.

This is still an immature funding mechanism, with bugs to be worked out. Many incubators are on the "liquidity event track" themselves...

How we fund companies will continue to change over the coming months.

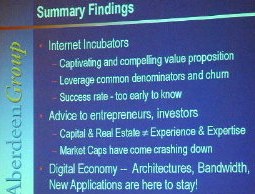

His final slide

Aberdeen Group has a full report ($2,500) on Internet Incubators. See their web site.

Fast Company co-founder Alan Webber speaks about success

The other speaker at the Software & Internet Council's meeting was Alan Webber. Alan co-founded Fast Company, a "different kind of business magazine", after spending six years as the managing editor/editorial director of the Harvard Business Review. His talk, entitled "Success in the New Economy", covered a wide range of topics of things he's noticed over the last 5 years and was very well received.

Alan Webber, smiling before and giving his talk

Here are some points as I heard them (and was able to take notes about with my Palm and keyboard):

Fast Company is based in Boston. Most people don' t know that.

A major motivation: It's never been a better or more exciting time to be in business than today. Thanks to the Internet and all, everything is up for grabs.

Old: Tangible assets, size matters, brand takes time to develop, past is a predictor of the future, cutting costs is the main thing to learn about in business, there is "one right way".

Now: Speed over size, flexibility over history, intangible is more important than tangible. He remembers the day when Intel was a major company, yet it had fewer employees than AT&T had just laid off. Growth: Topline is the future.

Create your own way of doing business. He believes in the "Jerry Garcia School of Business". The Grateful Dead, Jerry's band, was the largest grossing rock band the year before he died. He said: Not better, not different, but making music that only we can make.

Not just speed and size, but also imagination. The Web is not just an application but a way of working. There will be the invention of multiple new markets, with more than one way to do markets and capitalism. Auctions, name your price, buying groups, etc., etc.

After the "correction" last month, there is a new turn of the wheel: Now it's only "the economy" not the "old" and "new" -- everybody has to play by the same rules.

Convergence in the way of working: Old companies need to be fast, new companies need to learn discipline.

He quoted some rules from an article about Avram Miller, who used to run Intel's investment fund:

Intuition rules. At Intel he had to make up numbers after deciding on something so he could sell ideas to others.

Decide now, analyze later. Learn from review after an action.

Iterate, iterate, iterate. Nobody gets it right the first time. "Everybody should open in New Haven" (as opposed to opening a play on Broadway without a tryout). We never get it right, we just keep iterating to get closer. Fast Company included the author's email address on all articles from early on, and they learned a lot from reader feedback.

Change hurts, indecision kills.

Tap the global brain pool. There are smart people in more places than the region where your company is.

Companies build their own coffins, and become victims of their own success. (The "innovator's dilemma".)

Alan was at a conference where John Chambers, head of Cisco, was speaking. Since Cisco had just that day become the highest market cap company, everybody asked him questions. Some things John said according to Alan:

Speed wins: Fast to market. Time to learning. Speed with which you spread ideas within your organization.

Metrics of speed: What gets measured is what gets done. A capital budget is less important than a time budget.

Talent wins. The best people win. Talent is the scarcest asset.

Alan referred to a McKinsey list of how to "brand" your company to attract talent. Your "brand" in the eyes of potential employees is good if:

You are a "blue chip" company, that is you look good on someone's resume.

Big risk/big reward: Work here and maybe you'll never have to work again (but maybe not).

"Blues Brothers": "We're on a mission from God". What you do here will be so memorable you'll be proud to tell your grandkids when they ask what you did during the great Internet rush. (Major project, great public service, etc.) (This is like the Peace Corps or the Moon Mission when I graduated college in the 1970's.)

"I've got to get a life": Companies with sane environments -- they close their doors at 6pm, etc. Companies like this often have very low turnover.

Alan then talked about reinventing leadership. People want less management and more genuine leadership. It used to be, judging by major business magazine covers, that leaders were all white guys looking to the right with a strong gaze, appearing like football coaches overpowering their team. No more. Talent wants people who are really smart and ask great questions to lead them. They want you to stand for something and not just make something. He evoked John Seely Brown of Xerox PARC: a leader makes meaning, not product.

About companies: Built to last vs. built to flip? Why are you doing this? Not just to get rich (which is a limited way to keep score) but the point is to test your own creativity and skills and create a team. Do something as good as you can do, and keep your integrity and values while doing it.

End of talk. Time for Q&A:

How does he define the "new economy"? Not about economics, but around different work practices and view of the individual.

Where does quality fit in? Industrial economy needed material quality. Now we need the quality of customer experience, such as on the web. New metrics are needed. Dell is a classic example. They have a series of metrics around customer experience: Getting it right the first time (packing a box), how fast they respond to a complaint, etc. Harvard Business Review had an article about "customer recovery" -- how quickly you make it right. Quality will be a major thing in the service economy.

For more information, and to read the stories he's quoting from, see the Fast Company web site.

|

|